The companies building artificial intelligence infrastructure are consuming a growing share of the world’s memory chip supply.

The bill is arriving in your next device upgrade.

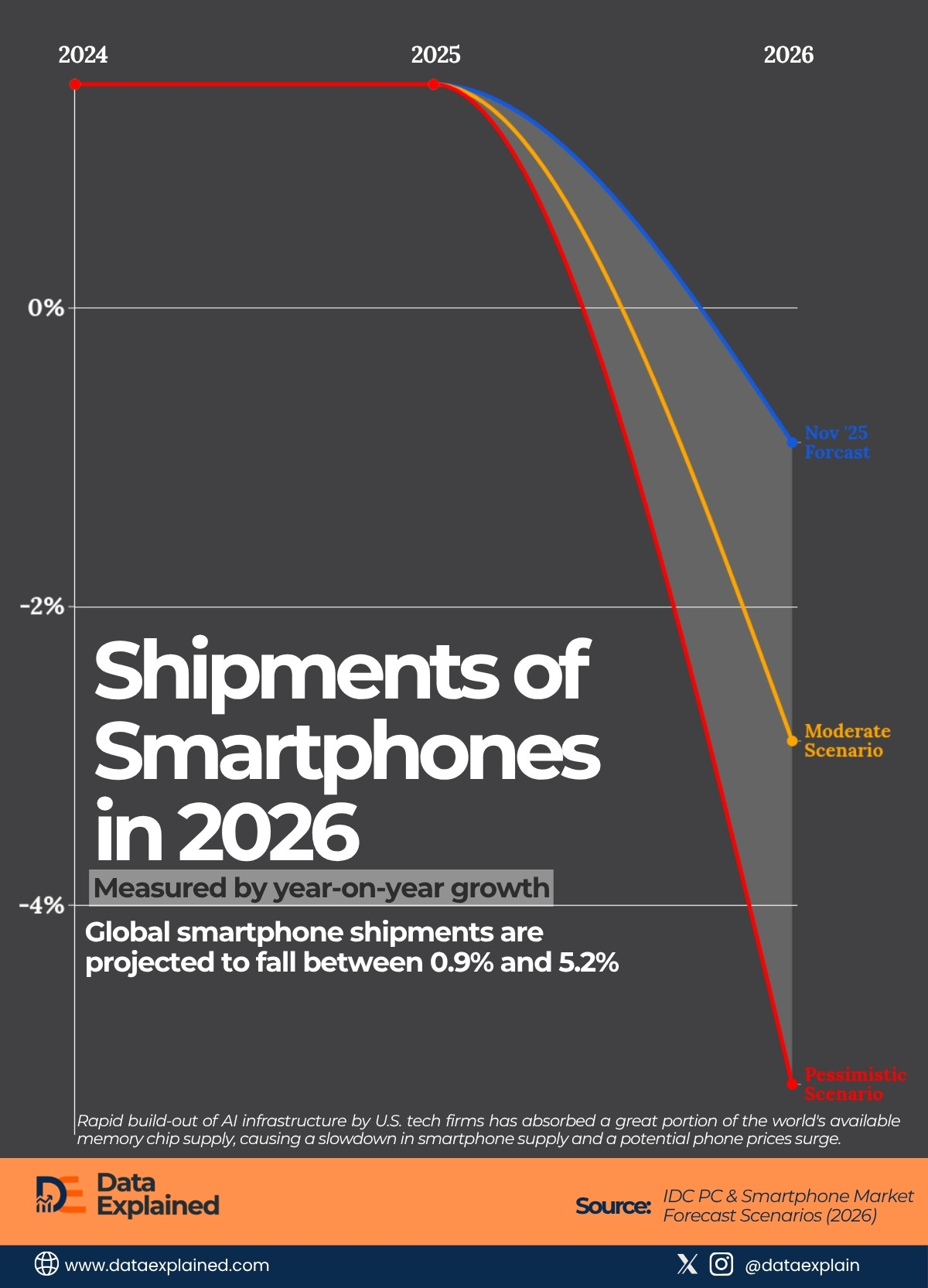

Today’s visualization shows a forecast of the smartphone markets based on projected unit shipments. The prediction is against two revised 2026 scenarios: Moderate and Pessimist.

TL;DR

- Global smartphone shipments are projected to fall between 0.9% and 5.2%.

- Global PC shipments are projected to decline by 2.4% to 8.9% in 2026.

The data comes from the International Data Corporation (IDC).

| wdt_ID | wdt_created_by | wdt_created_at | wdt_last_edited_by | wdt_last_edited_at | Year | Nov \'25 Forcast | Moderate Scenario | Pessimistic Scenario |

|---|---|---|---|---|---|---|---|---|

| 1 | emmanuel-ashemiriogwa | 27/03/2026 09:48 PM | emmanuel-ashemiriogwa | 27/03/2026 09:53 PM | 2025 | 1.50 | 0.00 | 0.00 |

| 2 | emmanuel-ashemiriogwa | 27/03/2026 09:48 PM | emmanuel-ashemiriogwa | 27/03/2026 09:48 PM | 2026 | -0.90 | -2.90 | -5.20 |

How Data Centres Are Reaching Into Your Pocket

The mechanism is specific and traceable.

The rapid build-out of AI infrastructure by U.S. technology firms, including OpenAI, Alphabet’s Google, and Microsoft, has absorbed a significant portion of the world’s available memory chip supply.

DRAM and NAND flash (the types of memory used in everything from smartphones to laptops to gaming consoles) are the same component categories that data centres require in enormous volumes to run AI models at scale.

Chip manufacturers are facing surging demand from data centre operators who pay significantly higher margins than consumer electronics brands.

So they have prioritized production allocation toward that segment.

The result is a tighter memory supply and rising costs for device makers.

Those costs are being passed through to consumers.

- HP Inc, one of the world’s largest PC manufacturers, has announced price increases to offset the higher component costs.

- Raspberry Pi, the British company behind the $35 single-board computer used in schools and hobbyist electronics projects worldwide, has done the same.

Story Behind Today’s Visualization

IDC’s forecast scenarios cover both PCs and smartphones separately, making a specific methodological choice worth noting.

While we focus on the smartphone trend, neither market includes an optimistic 2026 scenario.

Each presents three data points:

- The November 2025 baseline forecast

- A moderate scenario

- A pessimistic scenario.

The debate IDC is modelling is not whether these markets contract in 2026. It is by how much.

For PCs, the spread is significant.

The moderate scenario projects a 2.4% year-on-year decline in unit shipments. The pessimistic scenario projects an 8.9% decline (a figure that would rank among the steepest annual PC market contractions outside the 2022 post-pandemic correction).

IDC is treating an 8.9% decline not as a tail risk but as a modelled base case under adverse conditions.

For smartphones, the range runs from -0.9% in the moderate scenario to -5.2% in the pessimistic case.

The moderate figure is deceptive in its smallness.

A sub-1% decline would mean consumers absorbed most of the price increases without significantly altering their upgrade behaviour.

A 5.2% decline would represent the worst annual contraction in global smartphone shipments since the pandemic-era supply chain disruptions of 2020 and 2021.

AI’s Self-Defeating Cycle

Artificial intelligence was meant to be the reason consumers bought new devices in 2025 and 2026.

AI PCs (machines built with dedicated neural processing units to run on-device AI features) were the PC industry’s primary marketing platform at CES 2025 and throughout the year.

AI-enabled smartphones, from Apple Intelligence on iPhones to Google’s Gemini integration on Android flagships, were framed as the most compelling upgrade argument in years for a saturated handset market.

The AI infrastructure build-out has undermined the economics of delivering on that narrative.

The same investment in data centres that is meant to power next-generation AI features is consuming the memory supply that makes those AI-capable devices affordable to produce at scale.

The device industry entered 2026 with AI as its primary upgrade pitch and a memory price environment that makes executing that pitch more expensive at every tier.

What the Scenarios Require

The gap between IDC’s moderate and pessimistic outcomes for 2026 is wide enough (6.5 percentage points for PCs, 4.3 for smartphones) to suggest the firm sees a genuine fork in the road rather than a narrow range of probable outcomes.

The moderate case holds if tariff pressures ease, memory supply allocation shifts back toward consumer devices, and manufacturers absorb some costs rather than pass them through.

The pessimistic case applies if those conditions do not materialise.

Sources:

IDC PC & Smartphone Market Forecast Scenarios (2026) |